Palantir (PLTR) has emerged as one of the world’s leading AI companies, developing powerful platforms like Gotham, Foundry, Apollo, and AIP. Since the beginning of this year, the company has doubled its value through strong earnings results, showing progress in AI. However, when the colors are divided on the current PLTR stock appeal, despite the stretched multiples I remain bullish on the stock. This belief is based on Palantir’s unique position in the AI revolution which is still in its early stages.

In this article, I will highlight and discuss recent developments regarding Palantir and explain why the current price premium is justified.

Palantir’s Rally This Year

Palantir’s stock has seen triple-digit gains this year, rising more than 140% to hit an all-time high. Several key factors have combined in recent months to fuel this impressive increase.

First, the company’s commercial business has experienced rapid revenue growth. In its Q2 earnings report, released on August 5, Palantir noted a 55% increase in business from the commercial sector, while government contracts increased by 24%. Another indication of strength is from Palantir’s margin rates. Palantir posted a 16% operating margin in Q2, up 1,400 basis points year-over-year, continuing its trend of increasing profits. Operating income increased significantly from $10.1 million in Q2 2023 to $105.3 million in Q2 2024.

Additionally, the mass adoption potential of Palantir’s Artificial Intelligence Platform (AIP) has emerged as a major catalyst. With AIP, Palantir has demonstrated a unique technology that I see comparable to Nvidia’s (NVDA) microchip. In Q2 alone, the company closed 27 deals valued at $10 million or more.

The final reason for the price increase is the inclusion of Palantir in the S&P 500 (SPX) index. The stock joined the index on September 23, strengthening investor confidence, especially among institutional investors.

Important Metrics Reveal Much About Palantir

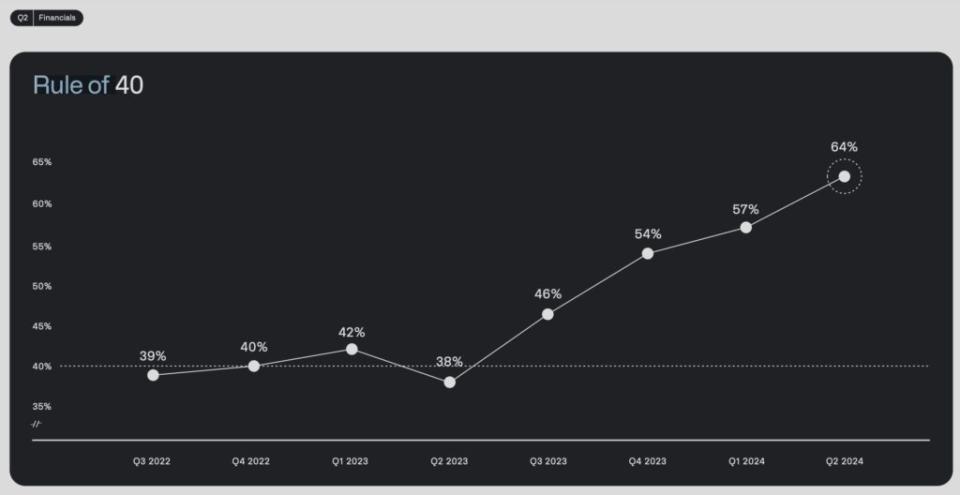

One of the main pillars of optimism about Palantir lies in the metrics that the company reported for the first time in the latest quarter: its status relative to Rule 40. The much-discussed Rule 40 shows that even SaaS (Software). as a Service) the company has less earnings today, it can still be a good investment if the revenue growth and profit margin percentage together total 40 or more.

During the Q2 earnings call, CEO Alex Karp highlighted that Palantir currently has a 40-point score of 64, with revenue growth of 27% and an adjusted operating margin of 37%. When it’s clear that Palantir outperforms the benchmark, how important is a score of 64?

When we compare Palantir’s Rule 40 score to other well-known SaaS companies, we can see that it stands out. For example, Adobe (ADBE) has a score of 51, Salesforce (CRM) has a score of 38, and CrowdStrike (CRWD) has a score of 37.

It’s worth noting that these companies have Palantir’s lower scores for various reasons, making it increasingly difficult to get a higher score. Companies with high Rule of 40 scores must maintain very high growth rates or very high operating margins. Most companies tend to excel in one area but not both. However, Palantir currently scores well in both components.

Analysts predict that Palantir’s revenue growth will continue to exceed 20% per year until at least 2027, which will support the company’s position against Rule 40, especially if its margins are at least unstable.

PLTR Stock Valuation: Key Points of Discussion

Arguably, one of the main things that separates Palantir’s bulls and bears is the company’s valuation. Undeniably, some traditional multiples have been stretched. Palantir trades at a forward P/E ratio of about 120x, which is more than double what Nvidia trades for, for context. Even if we adjust this variety for growth, using EPS growth forecast of 24.5% for the next three to five years, Palantir advanced PEG aspect above 4.8, compared to Nvidia 1.28. This is evidence of very optimistic market expectations for Palantir’s future.

Is this premium justified? I believe that paying a premium for stock is justified only when the company offers something uniquely valuable or disruptive. In the case of Palantir, from my point of view there is definitely something special. The company is a pure software provider, specializing in AI solutions for companies and government agencies. In CEO Alex Karp’s latest letter to shareholders, he highlighted the “constant wave of demand” from customers for production-ready AI systems, and Palantir is one company that can meet that demand now.

Because of these factors, I believe Palantir is uniquely positioned to expand the trillion-dollar AI market and gain a significant share of the enterprise software sector, which is expected to reach $790 billion by 2032.

Is PLTR Stock a Buy According to Wall Street Analysts?

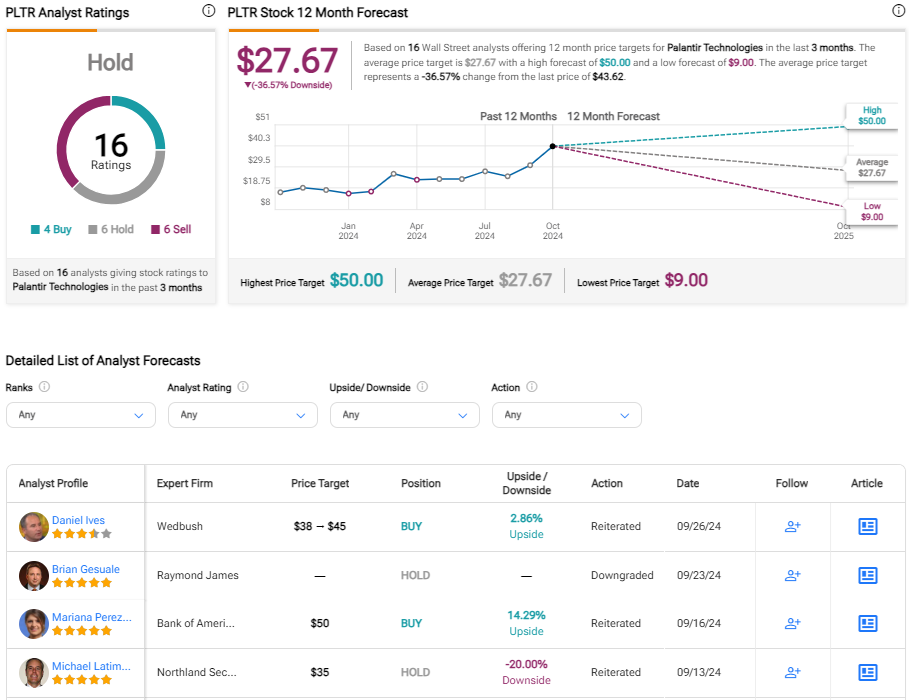

According to TipRanks, Wall Street analysts have a Hold consensus on PLTR stock. Among the 16 analysts who cover the stock, six recommend Hold, six suggest Sell, while only four advocate for a Buy. PLTR’s average price target is $27.67, more than 35% below the stock’s current price.

Conclusion

Although Palantir’s multiples may seem stretched for new investments at the moment, the premium price seems justified as the company positions itself as a unique AI pure play. The company’s strong results in the recent quarter confirm that the demand for the platform is high.

Additionally, key metrics like Rule 40 highlight Palantir’s distinct position among software companies, which is likely to continue and even strengthen in the long term. As a disruptive technology company, I believe PLTR stock’s premium valuation is warranted, although traditional valuation metrics may not capture the full value of the company. I remain bullish on PLTR stock.

disclosure

Disclaimer